Insights

Insights

An Interpretation of the Underlying Logic of the ESG Concept

Almost 20 years have passed since the term ESG was first coined in 2004, and ESG has gone from being a new phenomenon to a trillion-dollar business. According to statistics, in 2022, the total size of global ESG funds will have exceeded $2 trillion. Carbon neutrality, ESG and sustainable development have gradually become key concerns and widely discussed topics in the business community, and the good performance of ESG-related investments in the market has pushed the market, regulators, and enterprises to pay more attention to the link between ESG and long-term corporate development.

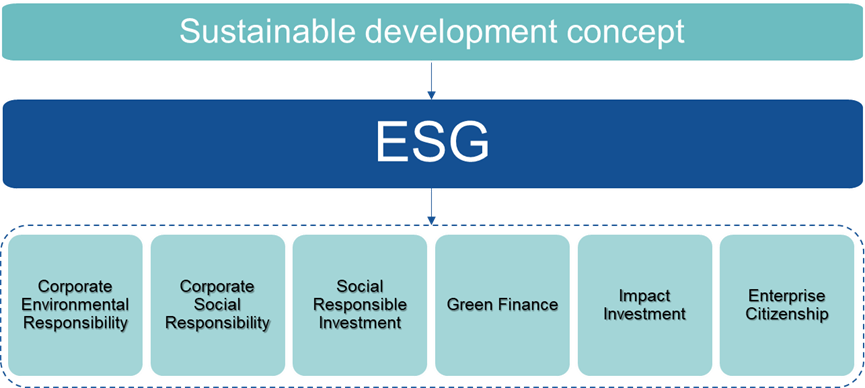

Sustainable development is a development concept

put forward by mankind since the 1980s to reflect on history and look forward

to the future, and it is also the general program leading the development of

human society at present. Enterprises, as the basic unit of human

economic activities, are an important and indispensable driver of sustainable

development.

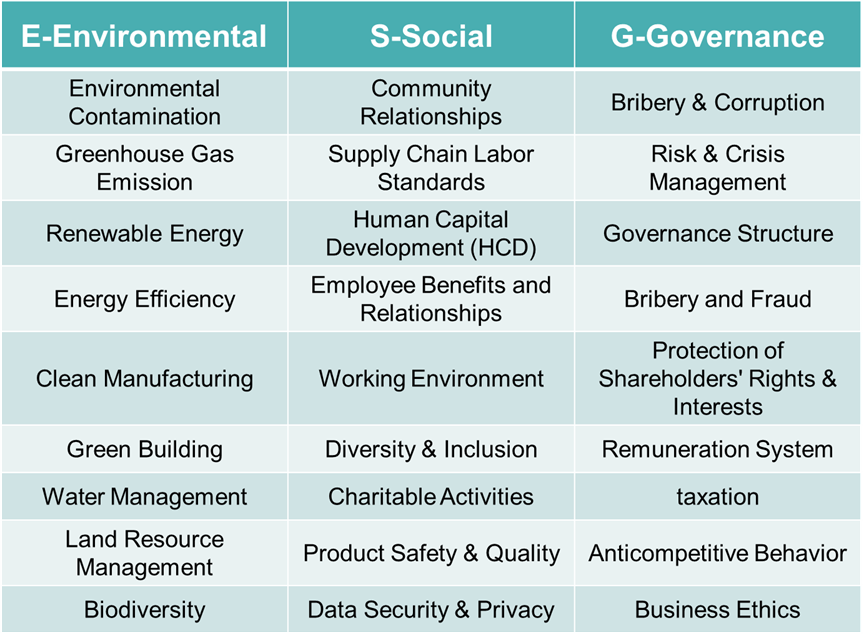

At present, despite the different opinions of various organizations on the setting of ESG indicators, the expressions of ESG connotation are relatively similar. Based on the generalization of the mainstream evaluation system, the common contents of the three ESG dimensions are listed in the table below.

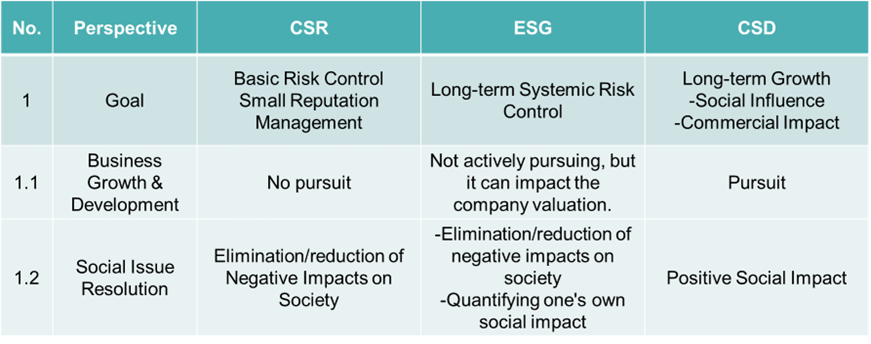

ESG and CSR (Corporate Social Responsibility), CSD (Corporate Sustainability Development) all represent the concept of businesses striving for goodness,While there may be some overlap in concept, the purposes of ESG, CSR (Corporate Social Responsibility), and CSD (Corporate Sustainable Development) are distinct. It is important for businesses to differentiate between them and understand the underlying logic behind their actions.

(1) Goal

CSR focuses on eliminating or reducing negative impacts, ESG does not actively pursue business growth and development, but the business prospects can affect the company's valuation. Additionally, the most significant characteristic of ESG is quantifying social impact. On the other hand, CSD aims for long-term business growth and increasing influence.

For example, in the case of an industrial company, if it actively seeks solutions to mitigate negative environmental impacts locally, it falls under the realm of CSR. When the company aims to quantify these actions as social impact and publicly disclose them, it falls within the scope of ESG. Lastly, when the company begins to formulate climate change and transition strategies, set climate goals, and proactively adjust supply chains and production lines to secure future business growth, it falls under the realm of CSD.

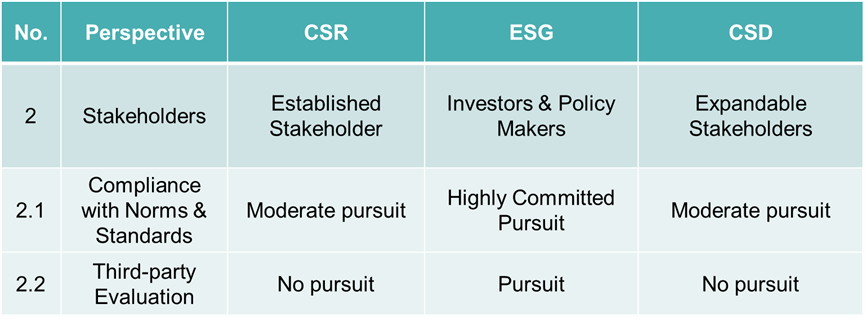

(2) Stakeholders

The concept of ESG itself has clear objectives, aiming to enable investors and policymakers to make comprehensive risk assessments of companies' non-financial information from the dimensions of environment, social responsibility, and corporate governance. Therefore ESG is the most important to pursue standards and norms compliance as well as third-party evaluation and rating.

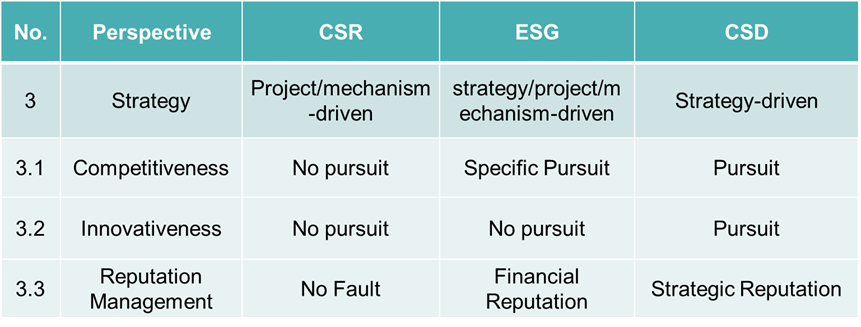

(3) Strategy

CSR is mainly project or mechanism

oriented, does not pursue competitiveness and innovation, and is more

conservative in reputation management, pursuing no-fault; ESG adds strategic

orientation to CSR and pursues rating improvement and reputation management;

CSD is mainly strategy oriented and pursues competitiveness, innovation and

strategic reputation at the same time.

It can be seen that CSR serves as the minimum ethical constraint on businesses. ESG is an assessment mechanism driven by specific goals, emphasizing compliance with certain norms and standards, continuously seeking higher third-party evaluations, eliminating negative social impacts through quantification, enhancing financial reputation, and attracting more investors. CSD represents the highest comprehensive value pursuit for enterprises and is the strategic orientation for long-term survival and development.

The ESG framework primarily consists of three key

elements: ESG disclosure, ESG evaluation, and ESG investment. Companies choose

an appropriate evaluation system, disclose relevant information based on the

evaluation system, evaluation agencies assess the disclosed ESG information of

companies, and investors make investment decisions based on the evaluation

results.

(1) ESG disclosure

ESG disclosure, also known as ESG information disclosure, includes mandatory disclosure and voluntary disclosure. Currently, in most countries or regions, ESG information disclosure remains voluntary for companies. It is up to the discretion of the companies whether to disclose, what information to disclose, and how to disclose it. However, a few countries or regions have started to introduce mandatory disclosure of specific ESG factors into their local laws and regulations.

Tips: ESG Disclosure System

As of 2023, a total of 69 stock exchanges globally have issued guidance documents for reporting, primarily referencing internationally recognized standards. According to incomplete statistics, the commonly used international standards include:

Up until now, there has not been a globally unified ESG disclosure standard. On June 26th, the International Sustainability Standards Board (ISSB) officially released the ESG Disclosure Standards. It is the first global sustainability reporting framework, and its publication is expected to further facilitate the development of a globally unified ESG disclosure standard.

(2) ESG Evaluation

ESG evaluation is an assessment method that considers environmental, social, and corporate governance factors as key considerations for investment evaluation. It involves categorizing, quantifying, and integrating ESG-related information and primarily encompasses indicator construction and scoring. Institutional investors incorporate ESG evaluation into their investment decision-making process to enhance portfolio risk management capabilities and improve long-term returns.

(3) ESG Investment

ESG investment involves considering environmental, social, and governance factors alongside financial factors in investment decision-making. It is a strategy based on ESG evaluation. Common approaches used by investors include negative screening, positive screening, norm-based screening, ESG integration, sustainable investment, impact investment, and others.

ESG is the emerging direction in corporate management and financial investment in the world today, particularly in Europe and America, where it is rapidly growing and evolving towards standardized and orderly practices.

For a country, ESG aligns naturally with China's

path towards high-quality economic development

For a country, ESG aligns naturally with China's

path towards high-quality economic development

The concept of "high-quality development" was first introduced in the report of the 19th National Congress of the Communist Party of China in 2017. It highlighted that China's economy has transitioned from a phase of high-speed growth to a phase of high-quality development. In the 14th Five-Year Plan (2021-2025), it is explicitly stated that China will steadfastly implement the new development philosophy of innovation, coordination, green development, openness, and sharing and promote high-quality development. Enterprises play a crucial role as the fundamental units in the operation of the economy and society.

The ESG concept emphasizes that enterprises should focus on ecological environmental protection, fulfill social responsibilities, and improve governance standards, which naturally aligns with the theme of high-quality development. Theoretically, ESG can provide guiding principles for enterprises to develop in the three aspects of environment, society, and governance, thereby indicating a pathway for high-quality development. In practice, ESG offers methods and indicators to evaluate the performance of enterprises in the three areas of environment, society, and governance, providing necessary tools for practicing high-quality development.

Moreover, the wide range of indicators covered by ESG and the "new development philosophy" of innovation, coordination, green development, openness, and sharing, along with the "30-60 target," are highly compatible. They can provide practical leverage for enterprises to implement the new development philosophy effectively.

For companies, poor performance in ESG evaluations

may constrain international capital inflows

Currently, the performance of Chinese companies in ESG evaluations by different rating agencies is not satisfactory. Chinese companies account for over 40% in both the MSCI and FTSE Russell Emerging Market Indices, which is proportional to China's level of economic development. However, in contrast, Chinese companies have a much lower representation in the ESG indices for emerging markets, falling behind Indian companies. In the FTSE Russell ESG index, FTSE4Good, which uses a 5-point scoring system, Chinese companies have an average score of 1.5, while the average score for emerging market companies is 2.1, and for developed country companies is 3.

Apart from the preference of international investment markets for sustainable companies, the low representation of Chinese companies in ESG-themed indices will also affect international capital inflows into these companies. As Chinese companies seek international expansion and long-term sustainable growth, they cannot afford to ignore ESG considerations.

ESG is the tangible manifestation of the concept of sustainable development within companies and aligns closely with China's philosophy of high-quality development. Currently, China is still in the early stages of ESG implementation and should draw on the experiences and lessons from the development of ESG practices abroad. By leveraging its latecomer advantages, China should focus on advancing ESG practices effectively. Only by accelerating the green and low-carbon transition, integrating the creation of social value with improved corporate governance, can ESG truly become a powerful tool for serving China's economy and promoting high-quality development of enterprises.

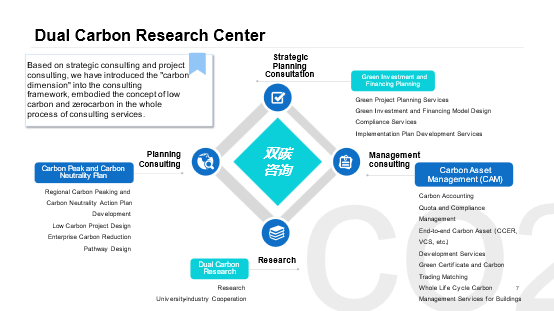

Double Carbon Research Center, Empowering Low-Carbon Consulting

.png)

The Double Carbon Research Center is rooted in the engineering consulting industry, introducing the "carbon dimension" into its consulting framework. It explores the fusion of "carbon + engineering" in service offerings and delves deep into the forefront of digitalization and decarbonization. By embodying the concept of double carbon throughout the entire service process, the center aims to facilitate efficient industry-academia research collaboration, leading the industry's digital and ecological development. The ultimate goal is to contribute to the realization of the 3060 targets through the strength of enterprises.

We will contact you within 24 hours.

EN

EN